Cash flow forecasting is the lifeline your business didn’t know it needed.

Running out of cash without warning? Struggling to plan big moves? With the right forecast, you can predict, prepare, and grow without panic.

This blog shows how smart forecasting can end cash chaos, unlock control, and fuel confident growth.

Read on to take full control of your cash flow.

Cash flow forecasting predicts how much cash you’ll have in the future. It estimates money in and out based on expected income and expenses.

You estimate how much money will come in (sales, loans) and go out (bills, salaries). You can forecast for a week, month, or even a year. It keeps your business from running dry.

Think of it like mapping a road trip. You don’t just start driving; you check fuel, pit stops, and the weather. Forecasting does that for your cash. It prepares you for bumps ahead.

Whether you're a startup or an enterprise, forecasting keeps you ready.

Cash is more than just a metric, it’s the engine that keeps a business running. Even highly profitable companies can face failure if cash flow isn’t managed properly.

|

According to Intuit’s "The State of Small Business Cash Flow" survey conducted in 2018, 61% of small businesses around the world struggle with cash flow, and nearly a third are unable to pay vendors, loans, themselves, or their employees due to cash crunches. |

That’s where cash flow forecasting steps in, offering a proactive way to prevent shortfalls and ensure financial stability.

Imagine you're a small manufacturer. You’ve landed a big order but payment is 60 days away. Meanwhile, your rent, salaries, and material costs are due next week. Without a forecast, you'd be blindsided.

With cash flow forecasting, you’ll see the gap in advance. That gives you time to extend credit terms, request a part payment, or delay non-urgent expenses.

Say you're running a marketing agency and want to hire a new account manager. Instead of guessing if you can afford it, a three-month cash forecast shows a dip in liquidity starting next month.

That insight helps you delay hiring or take on more retainers first. Forecasting keeps your growth plans aligned with actual financial capacity.

Picture this: you’re pitching to an investor for a ₹50 lakh seed round. Instead of vague projections, you present a 12-month cash flow forecast, showing how their funds will be used and when the business will reach cash-positive territory.

This transparency makes you look credible and well-prepared, exactly what investors want to see.

You run a retail store. Diwali season is coming, and you need to stock up inventory. With a forecast, you know your incoming cash will dip in October due to supplier payments. So, you negotiate better payment terms now or plan a sale in September to boost cash reserves.

That’s smart planning made possible by forecasting.

A well-structured cash flow forecast gives you a financial roadmap. It answers three key questions:

At its core, a forecast follows this simple formula:

Closing Cash Balance = Opening Cash Balance + Cash Inflows – Cash Outflows

Let’s break down what goes into each part:

These are the funds you expect to receive during the forecast period.Typical inflows include:

But inflows aren’t just about how much; timing matters. Knowing when the money will hit your account helps you avoid shortfalls between billing and collection.

These are your outgoing payments; planned or recurring. Common outflows include:

Also factor in seasonal expenses, bonuses, or large one-time purchases. Missing these can make your forecast inaccurate.

Your forecast should begin with the opening cash balance, the amount in your account at the start. Then, after subtracting outflows from inflows, you get the closing cash balance.

|

Quick Cash Flow Example: That ₹3,00,000 is what you'll have left at period-end—your liquidity cushion. |

Get clarity with the right forecast components.

Schedule your 1:1 callDifferent business goals call for different cash flow views. Whether you're planning next week's payroll or next year’s funding round, the forecasting timeframe you choose directly impacts your decision-making.

Here’s how to align your forecast with your business needs:

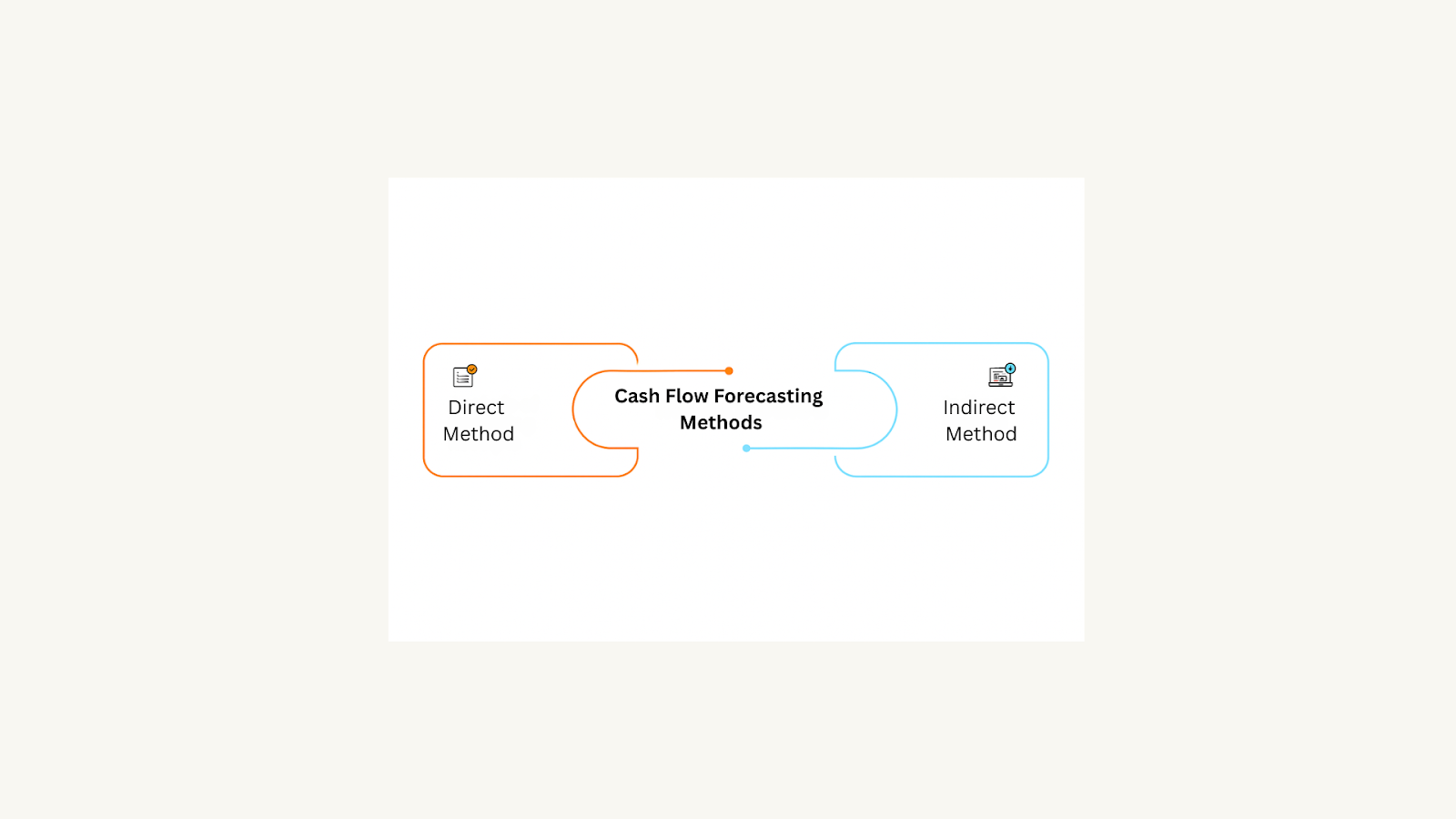

Choosing the right cash flow forecasting method depends on your goals, business size, and how accurate you want the forecast to be. Let’s look at the top three approaches:

This method is used in preparing Cash Flow Statement which tracks actual cash coming in and going out in real time. You list specific cash receipts and payments like customer invoices or vendor payouts.

It’s simple, highly intuitive, and often used in tools like Excel or Google Sheets.

Ideal for:

Think of it as a checkbook-style forecast—practical and hands-on.

The indirect method is used in preparing Cash Flow Statement which begins with your net income from the profit and loss statement. Then, it adjusts for non-cash items like depreciation, changes in working capital, and tax impacts.

This approach gives a higher-level view and is widely used in ERP systems like NetSuite, Oracle, and SAP.

Perfect for:

It’s accountant-friendly and preferred for internal reviews.

Contact us to get your cash flow forecasting done

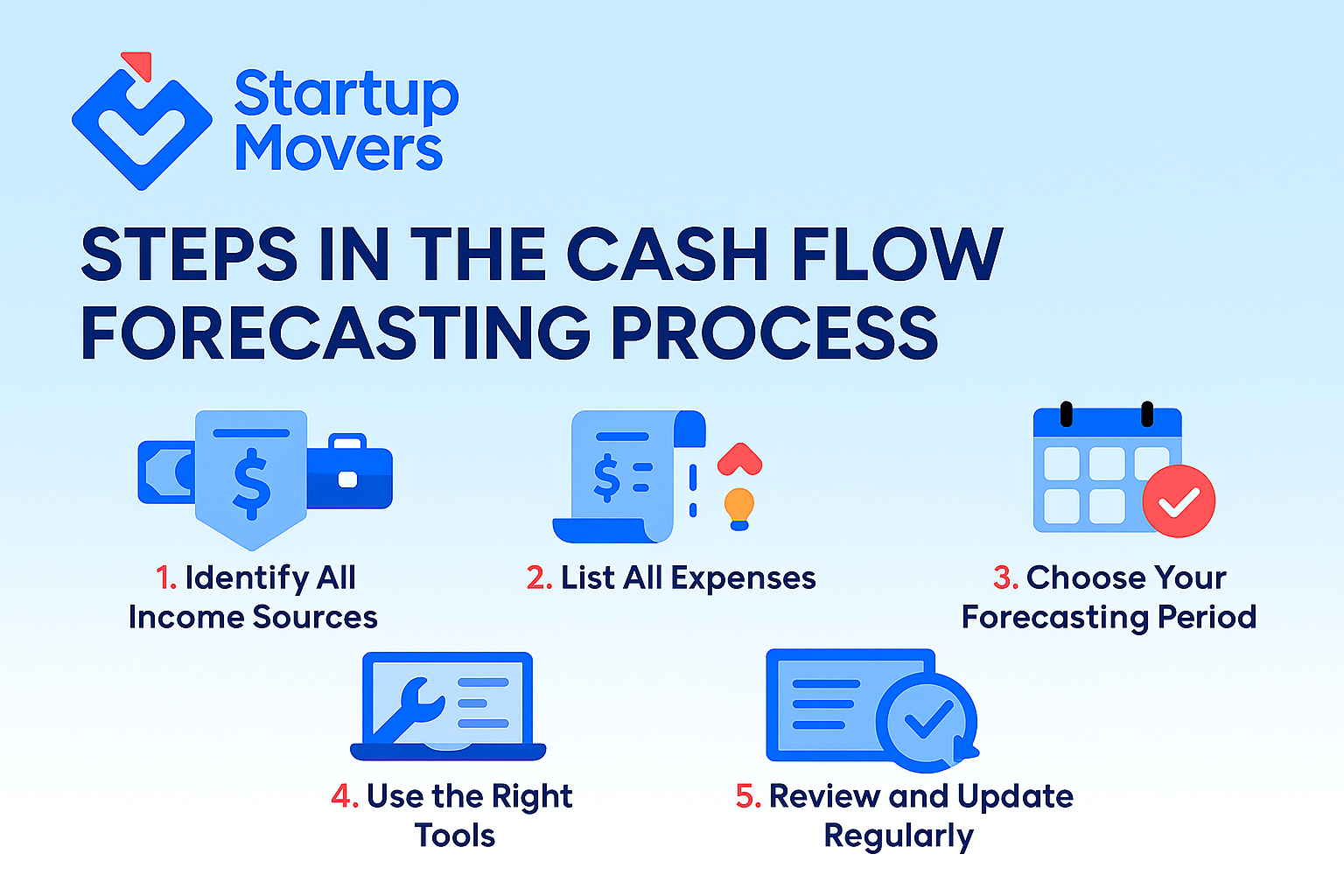

Schedule your FREE callBuilding a reliable forecast doesn’t require a finance degree. Just follow these five practical steps:

Start by listing every source of incoming cash. This includes customer sales, loan disbursements, tax refunds, grants, or investor funding.

Be realistic. Don’t count cash until it’s expected to land in your account.

Break down every expected payment. Include:

The more detail you add, the more accurate the forecast.

Pick a forecasting window that fits your planning needs. Short term (weekly), medium term (quarterly), or long term (annually).

Start small if you're new, like a 30-day forecast and build up.

If you're just starting out, try cash flow forecasting in Excel. It’s simple, flexible, and easy to customize.

Many startups use Excel templates before moving to advanced tools like Float, G Treasury, or Zoho.

Your forecast isn’t a one-time task, it’s a living document. Update it monthly (or even weekly) to reflect:

Staying current helps you stay in control.

Negative cash flow can happen, even in profitable businesses. The key is understanding why it’s happening and whether it's a short-term dip or a long-term threat.

Sometimes, negative cash flow is part of the plan. For example:

These may create temporary shortfalls but they’re backed by growth strategies.

If cash keeps bleeding with no plan to reverse it, that’s a red flag. Examples include:

When your outflows regularly exceed inflows, it threatens solvency.

In 2023, a fast-growing tech startup in Mumbai expanded aggressively. They opened three new offices and doubled their team, without monitoring burn rate.

They ran out of funds in eight months. By the time they started fundraising, it was too late.

A proactive cash flow forecast could have warned them months earlier.

Forecasting isn’t just number-crunching, it’s about creating clarity. Follow these tried-and-true tips to sharpen your process:

Forecast cautiously:

This builds a cash buffer and avoids unpleasant surprises.

Build three versions of your forecast:

Scenario planning helps you prepare, not panic.

Cash flow forecasting is your financial early warning system. It helps you avoid shortfalls, plan confidently, and build long-term stability.

As your business grows, consider leveraging tools or even a Virtual CFO to level up your forecasting and financial planning.

Start simple, review regularly, adjust often.

Because with clear visibility, you’re not just surviving, you’re leading with confidence.

Q. What is the principle of cash flow forecast?

The core principle is visibility. It tracks future inflows and outflows to avoid cash gaps. Forecasting supports better decisions and financial control.

Q. What is a three-way cash flow forecast?

It combines your cash flow statement, P&L, and balance sheet. This gives a complete view of cash, profits, and assets together.

Q. What are the advantages and disadvantages of cash flow forecasting?

Advantages: Better planning, investor confidence, fewer surprises

Disadvantages: Based on estimates, needs updating, not 100% accurate

Q. What are common cash flow forecasting challenges?

Inaccurate data, delayed payments, unexpected costs, and manual errors. Tools help reduce risks.

Get a virtual CFO to ensure apt cash-flow forecasting.

Schedule your 1:1 call

Published Date: 02 Jul 25

© 2025 Startup Movers Private Limited. All rights reserved. | Designed By : The Night Marketer

Leave a Comment

Comments

No comments yet.

RECENT ARTICLES

How to close a Registered Company? Step By Step Procedure!

GSTR-9 Annual Return: Complete Guide

Angel Syndicates in India (2025): How They Work for Early-Stage Founders?

Difference between Winding up and Strike off a Company

What is ESOP Meaning, Benefits & How do ESOPs Work?

Unlock Business Subsidy with PMEGP for Startups (2025)

AI Startups in India: Opportunities, Challenges & Compliance Guide (2025)

What is Bookkeeping & its Process?